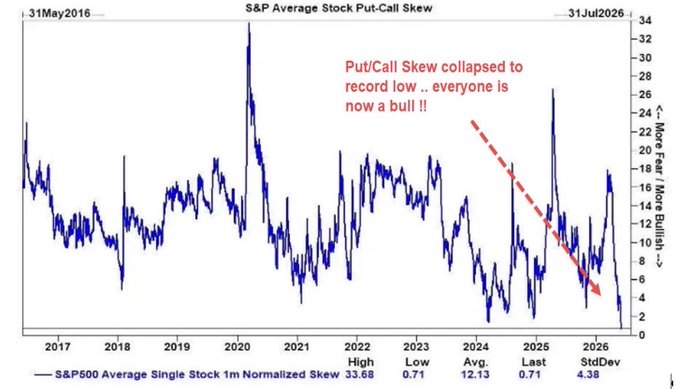

Lo skew put/call dell’S&P è appena crollato a 0,71. Non un minimo. Il minimo registrato di sempre. La media decennale è 12. Nel panico del 2020 ha raggiunto il picco a 34. Cosa misura: quanto pagano gli investitori per proteggersi da un crollo rispetto a scommettere su un rialzo. A 0,71, la protezione dal crollo è essenzialmente gratuita. Nessuno la vuole.

Il mercato delle opzioni prezza l’hedging come un’assicurazione su una casa che non può bruciare. Nessuno compra assicurazioni al massimo. – The S&P put/call skew has just collapsed to 0.71. Not a low. The lowest ever recorded. The 10-year average is 12. In the 2020 panic, it peaked at 34. What it measures: how much investors pay to protect against a crash relative to betting on an upside move. At 0.71, crash protection is essentially free. Nobody wants it. The options market is pricing hedging like home insurance on a house that can’t burn down. Nobody buys insurance at the top.